AMIFA Blog

COVID-19 Update

Just to let you now that during this virus, social distancing doesn't allow us to meet clients face to face.

However, we are taking Will instructions over the telephone and via video (Whatsapp).

We are also able to do same for Powers of Attorney(LPA's)

Please call on 01443 684007 or 07861216474 if you need to discuss your requirements.

#staysafestayhome

Now extended to Armed Services as well! £200 off all Silver Clouds Funeral Plans for all Police, Fire and NHS staff!

This offer is available to all staff in Fire, Police and NHS - currently serving or retired. Now includes Armed Services.

Silver Clouds funeral plans start from £2,250 for their direct cremation while their most popular traditional plan is £3,575 - these prices are before the £200 discount.

Instalment plans are available and are interest free up to 3 years.

Retirement Planning

Over 55? ISA or Pension?

One of the main aspects of a pension that has been off-putting to savers was the inability to access the money. However, with the introduction of pension freedoms, savers are able to take income as and when they require after the age of 55.

Saving via a pension can also be beneficial from an estate planning point of view in a way that ISAs are not. Money purchase pensions are outside of the estate for inheritance tax and thus a highly efficient method of passing on wealth to your children.

Deciding between a pension and an ISA will ultimately depend on your individual circumstances, and in many cases a combination of ISAs and pensions should be used together as part of a financial plan.

The above has been provided for information only and should not be construed as advice.

Pre Paid Funeral Plans

Are All Funeral Plans The Same?

FREE Will or £50 M&S giftcard with all plans

You'd think that a funeral plan is just that; a plan that pays for your funeral, however, after extensive research AMIFA has found that they are not. If the right plan is not chosen at outset your estate may have to pick up an extra cost at the time of your death and even a sub standard service.

Most people want to have their choice of funeral director, maybe because they have been used by the family over the years. Not all funeral plans guarantee this.

Secondly, most funeral plans are costed up with a cremation as the main choice for the funeral and they set aside an amount to go towards the funeral. Depending upon where you live this may not be enough if you wish to be buried and your estate will be called upon at the time of need to make up the difference.

If you are considering taking out a pre-paid funeral plan get in touch to discuss your options now.

For every funeral plan taken out you have the choice of a FREE will or a £50 M&S gift card.

Taxman Helps Pay Your Life Cover

Are You a Company Director With Life Cover?

Beware!

Lasting Power of Attorney and Joint Bank Accounts

There has been much debate recently about whether or not a Power of Attorney is relevant where people own joint bank accounts. There is a general misconception that when one party loses capacity the party who still has capacity can still access the funds.

HOWEVER, THIS IS INCORRECT!

The British Bankers' Association guidance states that when dealing with a joint bank account where one party has lost capacity the bank can decide whether to temporarily restrict the account, unless or until there is Power of Attorney or deputyship in place.

Claiming Mortgage Interest Relief on Let Properties - Are You Doing It Right?

3 years later the property is valued at £150,000 and you increase your mortgage on the property to £115,000. All of the interest on the mortgage can still be claimed as a revenue expense as the loan doesn’t exceed the initial £120,000 value of the property when it was introduced to your letting business.

If you increased the mortgage to £125,000, the interest payable on the additional £5,000 is not tax deductible and cannot be claimed as a revenue expense.

The capital raised can be used for any legitimate purpose even if unconnected to the letting business, for example, to pay off some or all the mortgage on your residential home or purchase a car.

If you have a portfolio of mortgaged buy to let properties you could remortgage raising small amounts from each to provide a substantial amount for personal expenditure or additional properties, all helped by the tax man!

Need further advice - get in touch.

How Long Do You Need To Keep Your Tax Documents?

How Do You Store Your Will?

Your Will is an important document and the one you have signed is the ONLY legally binding will.

Scans, photocopies and other representations are not legally valid because they don’t have your original signature on them.

If your Will gets damaged by fire, water, mildew, pests etc then it could be declared invalid.

You should keep your Will in a secure place, however that place must be easily accessible when the document is needed.

If your will is lost or damaged in your lifetime you may not be able to make a new will, for example, if you lose mental capacity.

In addition, a charge would be made to make a new will.

AMIFA Limited use National Will Safe to protect your Will.

The annual cost is £25 taken by direct debit.

· Your documents are stored in waterproof wallets

· Stored in a specialist document archive

· Documents are fully insured

· Documents can be returned to you or AMIFA Limited – free of charge

· Documents can be returned to Executors when needed – free of charge

· Documents are scanned and stored electronically acceptable to the courts

· Documents are recorded on the National Wills Register

· Plastic identity cards are provided for you and your executors with a telephone number for National Will Safe and a unique reference number.

Please get in touch if you wish to store your wills and other important documents.

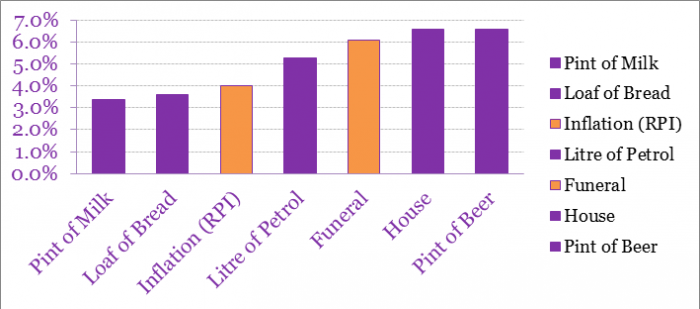

Funeral costs in Wales are rising faster than anywhere else in the UK according to insurer Royal London.

Wales has seen annual increases of 5.2% compared to UK average of 3.9%

The mutual insurer says, given the price rises it is not surprising to see funeral debt rising in UK households. A survey of 2,000 people by YouGov found more than one in ten people (13%) struggle to pay for a funeral today. On an individual level, funeral debt is £1,318 - collectively, across the UK this equates to £98.9m.

They say to cope with rising costs people are cutting-back when it comes to paying for essential items such as coffins, and optional elements such as flowers. The most striking example is coffins: last year’s Index found people spent £1,108 on average, but the 2015 report shows this has dropped to £989, a decrease of 11%. People are also exploring alternative burial options - 8% are now ‘woodland’ or ‘‘natural’

With average savings rates of less than 0.5% now is the time to lock in the cost of your funeral by arranging a prepaid funeral plan with AMIFA.

We have a range of options available from less than £2,000, payable in full or monthly installments including the UK's only GREEN environmentally friendly funeral plan.

Ashes to Ashes......David Bowie was cremated without a funeral or any family and friends present. The iconic singer told his loved ones he wanted to “go without any fuss” and not have a funeral service or public memorial.

Many people are considering this option now. This is the simplest of all funerals and meets the needs of a growing number of people who want a respectful direct cremation arranged without any fuss and leaving them free to say farewell how, where and when is right for them.

AMIFA Limited can now offer this service having researched the market and identifying a top funeral plan provider for this service.

Who chooses this type of funeral?

- People who firmly believe that a funeral should be a simple physical disposal

- Families for whom a separate Memorial Service is more important and appropriate

- Individuals who have no close family

- Relatives who face big challenges in coming together for a funeral ceremony

- Those who just want a cremation without a funeral service

- Those looking for a no fuss funeral

- Families searching for the cheapest funeral

If you are considering this type of funeral it is important to discuss your plans with your family to let them know your wishes.

As 'cremation only' doesn't include any ceremony at all we would be happy to help your family find a meaningful way to say goodbye and suggest different ways to remember you.

The cost of a 'direct cremation' funeral is £1,745 and can be paid in full or installments over 12-60 months.

If you would like to discuss it please get in touch with us on 01443 684007

Are You Claiming The Marriage Allowance?

Funeral costs soar by 10 times the increase in the cost of living in a year – forcing families to cut corners on their loved ones’ send off

The overall cost of dying which includes death-related costs such as probate, headstones and flowers in addition to the basic cost of a funeral - has risen by 8.3% to £8,802.

The funeral - which makes up 44% of the cost of dying - has soared by 5.5% in a single year. The average funeral in the UK now costs £3,897 which is more than double what it was when SunLife first started tracking funeral prices in 2004

This year, more than three in five (62%) put at least some money aside compared to 59% last year and just over half (54%) in 2009.

And while this is definitely encouraging, it still means that 38% are still making no provision to pay for their own funeral. Of those that do make some provision, one in five are not leaving enough to cover the full cost, up from one in six last year.

Shouldn't you make your arrangements now with a pre-paid plan? Click here